What is a Lady Bird Deed in Florida?

A Florida Lady Bird Deed – formally known as an Enhanced Life Estate Deed – is a powerful but straightforward planning tool that lets you keep full control of your home during your lifetime while automatically passing it to your chosen beneficiaries when you die.

Think of it as a “Transfer on Death” deed for real estate: your home passes to your family cleanly and quickly, bypassing the time and expense of Florida probate – because of this, it has become one of the most popular estate-planning moves for Florida homeowners as a result.

The 4 Core Benefits of an Enhanced Life Estate Deed

Florida homeowners choose an Enhanced Life Estate Deed for four key reasons. Here is what this deed can do for you and your family:

1. Total Probate Avoidance

Florida probate can be slow and expensive. A properly drafted Lady Bird Deed allows the owner’s interest to pass to the named beneficiaries (remaindermen) at death without a probate deed for that property.

- Immediate Transfer of Title: Unlike assets handled by a Will, which generally must be administered through probate, a properly drafted and delivered Lady Bird Deed can cause the remainder interest to become effective at death. Your heirs typically record your death certificate in the public records of the county where the property is located (such as Palm Beach County or Martin County) to update or “perfect” the title record.

- Reduction of Probate Costs: By keeping the home out of a Florida formal administration, your family may avoid probate court costs and attorney fees for one of your largest assets.

- Privacy Considerations: Probate is a public process where assets, debts, and court filings may become part of the public record. A Lady Bird Deed may avoid probate for the home, keeping it out of that public process, just keep in mind that the deed itself and other land records are generally public record.

2. Medicaid Asset Protection

Some deeds can trigger a Medicaid “transfer penalty,” but Florida generally treats a properly drafted Enhanced Life Estate Deed differently because the owner retains broad powers over the property.

- 5-Year Look-Back Planning: Because a Lady Bird Deed is revocable and the owner retains enhanced powers, Florida Medicaid has generally not treated a properly drafted deed as a completed divestment for look-back purposes. Eligibility still depends on the owner’s full financial facts, current Medicaid rules, and proper drafting, so it should be reviewed before recording.

- Medicaid Estate Recovery Planning: Florida Medicaid estate recovery is generally limited to assets that pass through probate. Because a properly drafted Lady Bird Deed can keep the home outside the probate estate at death, it may reduce estate-recovery exposure for that property. Results depend on current law, the owner’s eligibility facts, and the deed language, and Medicaid rules can change.

3. Retention of Homestead Rights

A primary concern for Floridians is losing the “accrued” tax savings they’ve built up over years of homeownership. The Lady Bird Deed is designed to leave these protections undisturbed.

- “Save Our Homes” Stability: During the owner’s lifetime, a properly drafted Lady Bird Deed is generally not treated as a current transfer that uncaps the owner’s Save Our Homes assessment limit. Post-death property-tax treatment may differ depending on who receives the property, whether a homestead exemption continues, and current property-appraiser rules.

- Homestead Portability: If you decide to sell your home later using your “enhanced” powers, your Homestead Portability may remain available during your lifetime if you otherwise qualify. This can allow you to transfer accumulated tax savings to a new Florida residence, but eligibility depends on Florida homestead rules and timing.

- Creditor Protection: During your lifetime, a properly drafted Lady Bird Deed generally should not disturb your Florida Homestead creditor protection. Your primary residence may remain shielded from many judgment creditors, but protection depends on constitutional homestead requirements, deed language, and the facts of the claim.

4. Absolute Freedom to Act

Unlike a traditional life estate, you generally do not need the consent of your heirs to sell the home, change beneficiaries, or use the retained powers stated in the deed. Legally, you hold an enhanced life estate with broad retained powers, while the beneficiaries hold a defeasible remainder that can be changed or defeated during your lifetime.

- Unilateral Power to Revoke: The most powerful feature of the “enhanced” life estate is your ability to revoke or change the deed at any time without notifying the beneficiaries. If your family dynamics change, you can simply record a new deed or a revocation document to cancel the previous arrangement.

- No “Joinder” Typically Required: In a standard life estate, your children (the remaindermen) own a future interest in the home. If you wanted to sell the property, they would usually have to sign the closing documents, and they might even be entitled to a portion of the sale proceeds. With a properly drafted Florida Lady Bird Deed, beneficiary joinder is usually not required for the owner to sell or otherwise use the retained powers, and the owner typically keeps the sale proceeds.

- Financing and Encumbrance Rights: You may retain the power to mortgage, encumber, or otherwise deal with the property, including through a HELOC or reverse mortgage, if the deed is drafted correctly. Lender, title-insurance, and reverse-mortgage underwriting requirements vary, so financing may still require lender review, beneficiary releases, or other title curative steps in some transactions.

Understanding the Risks and Drawbacks

The Lady Bird Deed is a powerful planning tool, but it is not the right solution for every situation. Here are the key limitations to understand before moving forward:

- Title Insurance Issues: Some title companies are wary of Lady Bird Deeds if they aren’t drafted perfectly. An error in the “powers” clause can “cloud” the title, making it difficult for you or your heirs to sell the property later.

- Multiple Beneficiaries: If you name multiple children as heirs, they must all agree on a sale price and sign the paperwork after you pass. If they disagree, it can lead to a “partition” lawsuit.

- Limited Protection for Heirs: Unlike a properly designed trust, a deed alone provides little or no spendthrift-style protection for your beneficiaries. If your heir has an IRS lien, creditor issue, or pending divorce when they inherit, their interest may be exposed. Naming a trust as a beneficiary may add protection only if the trust terms are drafted to provide it.

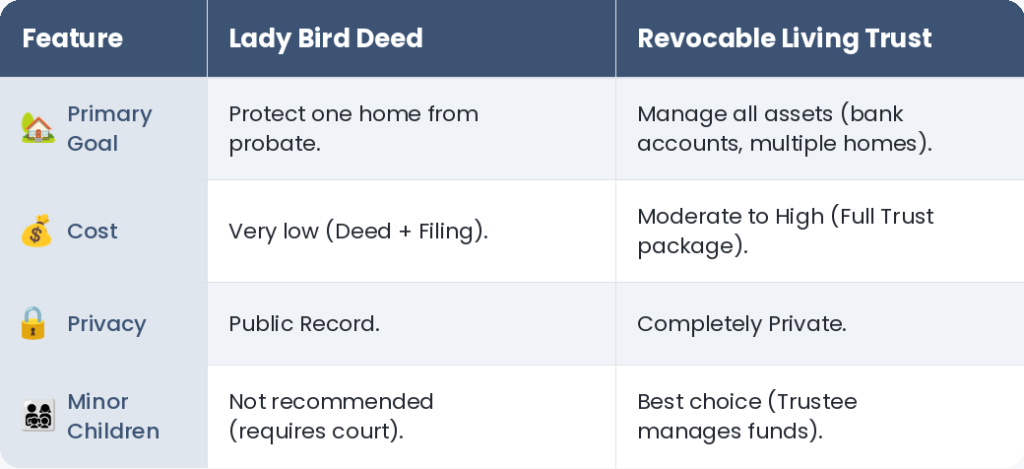

Lady Bird Deed vs. Revocable Living Trust

Not sure whether a Lady Bird Deed or a Revocable Living Trust is right for you? The best choice depends on the size and complexity of your estate. Here is a side-by-side look:

The Power Move: Why Not Both?

The good news is that you do not always have to choose one over the other. Many of our clients use a “hybrid” strategy: naming your Revocable Living Trust as the beneficiary of your Lady Bird Deed. This allows your home to bypass probate and flow seamlessly into your trust at death.

This may provide your heirs with spendthrift protection if the trust terms are drafted to do so, and it can allow a Successor Trustee to manage the property for minor children or beneficiaries who should not receive property outright, all while keeping your life simple while you are healthy.

How to File a Lady Bird Deed in Florida

Getting a Lady Bird Deed done correctly comes down to five essential steps. Whether you are starting from scratch or reviewing a form you found online, here is what Florida law requires for a valid, enforceable deed:

- Draft with “Enhanced” Language: You must include a clause reserving your right to sell, lease, mortgage, revoke, or otherwise deal with the property without the joinder of the beneficiaries.

- Verify the Legal Description: Use the legal description from your current deed, not just the street address.

- The 2+1 Execution Rule: You must sign and deliver the deed in the presence of two witnesses and one notary public, using the same formalities required for Florida deeds.

- Recording: Record the original deed with the Clerk of the Court in the county where the home is located (e.g., Palm Beach County or Broward County). Recording gives public notice and is usually essential for the probate-avoidance plan to work smoothly.

- Pay Fees: Expect a recording fee and potentially documentary stamp tax. A nominal amount may apply when there is no consideration and no mortgage, but the tax can be more complicated if the property is mortgaged, consideration is paid, or county recording practices require additional review.

Lady Bird Deed Florida Tax Consequences

One of the biggest reasons Florida homeowners prefer a Lady Bird Deed over a simple quitclaim deed is the potential to protect your family from unnecessary taxes. Here are the four tax areas you need to understand:

1. The “Step-Up in Basis” (Capital Gains Tax)

This is perhaps the single greatest financial benefit for your heirs.

- The Rule: When you name a beneficiary on a Lady Bird Deed and retain enhanced lifetime powers, the property is generally treated as passing at death for income-tax basis purposes. That may allow your heirs to receive a “step-up in basis,” subject to federal tax law in effect at the time and the facts of the transfer.

- The Potential Savings: If you bought your home in Palm Beach Gardens years ago for $200,000 and it is worth $800,000 when you pass away, your heirs may receive an $800,000 basis. If they sell it immediately for that same value and there are no other taxable adjustments, they may owe little or no capital gains tax.

- The Alternative: If you were to add them to a standard deed while you are alive, they may receive your original $200,000 carryover basis and potentially owe taxes on later gain, depending on the structure of the transfer and applicable tax rules.

2. Preservation of Homestead & “Save Our Homes” (Property Tax)

In Florida, your property taxes are protected by the Homestead Exemption and the Save Our Homes cap, which limits annual assessment increases.

- No Lifetime Reassessment: Recording a properly drafted Lady Bird Deed is generally not treated as a current “change in ownership” by the County Property Appraiser during the owner’s lifetime. Post-death reassessment and exemption treatment may differ depending on the beneficiaries and current rules.

- Continued Protection: During your lifetime, you generally retain your Homestead Exemption and constitutional homestead creditor protection as long as you live in the home as your primary residence and otherwise qualify.

3. Federal Gift and Estate Tax Considerations

Because a Lady Bird Deed is revocable (meaning you can change your mind at any time), the IRS treats the transfer differently than a standard gift.

- Gift Tax Return: Because the transfer is generally not treated as a completed gift when the owner retains enhanced powers, a federal gift tax return often is not required upon signing. Tax-reporting duties can depend on deed language, consideration, and then-current IRS rules, so tax advice is recommended.

- Estate Tax Inclusion: The value of the home will generally be included in your gross estate for federal estate tax purposes. For many Florida families, no federal estate tax is due because the estate is below the then-current federal exemption which as of 2026 is roughly $13.6 million.

4. Documentary Stamp Taxes (The Recording Cost)

When you record a deed in Florida, the state typically charges a Documentary Stamp Tax.

- Potential Minimal Cost: For many estate-planning transfers involving a Lady Bird Deed where no money is changing hands and no mortgage is involved, documentary stamp tax may be nominal. The correct amount depends on consideration, mortgage debt, and current Department of Revenue and county recording practices.

- Mortgage and Consideration Complexity: If there is a mortgage on the property, consideration is paid, or the deed is part of a larger transaction, the calculation can become more complex and should be reviewed before recording.

Secure Your Legacy

A Florida Lady Bird Deed is one of the most effective – and cost-efficient – tools available to protect your home and simplify your family’s future. But it only works as intended when it is drafted and integrated correctly into your broader estate plan. A single error in the “powers” clause or a missing provision can cloud your title and leave your heirs facing the exact legal headaches you were trying to prevent.

At Hale and Hodges Law, we take a comprehensive view of your estate – not just one issue or one document. Whether your priority is protecting your homestead, navigating Medicaid eligibility, or coordinating your deed with a Revocable Living Trust, our team provides the careful, personalized guidance that your family’s most valuable assets deserve.

Your home represents a lifetime of hard work. Do not leave what happens to it up to chance. Contact Hale and Hodges Law today to schedule your free estate strategy session – we will help you build a plan that protects it.

This article provides general Florida estate-planning information only. It is not legal, tax, Medicaid, or title-insurance advice, and results depend on the exact deed language, the owner’s facts, current law, lender and title requirements, and applicable agency rules.

Free Estate

Strategy Session

Enter your information below and one of our attorneys will contact you within 24 hours

FAQs

Do I need an attorney for a Lady Bird Deed in Florida?

While not legally required, it is highly recommended. Errors in a Florida Lady Bird Deed sample can lead to “latent defects” in the title. If the specific “enhanced” powers aren’t worded correctly, title insurance companies may refuse to issue a policy when your heirs try to sell the home, forcing them into a “Quiet Title” lawsuit that costs significantly more than a consultation today.

Does a Lady Bird Deed trigger a "Due on Sale" clause?

The federal Garn-St. Germain Act limits when a lender may enforce a due-on-sale clause for certain transfers of residential real property, including some transfers to a relative after death and certain estate-planning transfers where the borrower remains an occupant and retains rights. A properly drafted Florida Lady Bird Deed for a primary residence is often structured to avoid an immediate due-on-sale problem, but the answer depends on the loan documents, occupancy, property type, lender practices, and current law. Investment, commercial, reverse-mortgage, and HELOC situations should be reviewed before recording.

What happens if the beneficiary dies before the owner?

This is a critical risk of DIY deeds. If a beneficiary passes away first, their interest may lapse, pass under survivorship language to the surviving named beneficiaries, pass to that beneficiary’s descendants, or create probate/title issues, depending on how the deed is drafted. A well-drafted deed should say what happens if a beneficiary predeceases the owner and should include survivorship and/or “contingent beneficiary” language to help prevent the property from falling back into the probate system.

Can I use a Lady Bird Deed for property outside of Florida?

Lady Bird Deeds are only recognized in a handful of states (including Florida, Texas, and Michigan). If you own property in a state that does not recognize them, you may need a different strategy, such as a Revocable Living Trust, to avoid probate in that specific state.

Does a Lady Bird Deed protect the home from my own creditors?

It may preserve your existing Florida homestead creditor protection, but that protection comes from Florida’s Homestead laws, not the deed itself. While you are alive and the home qualifies as your primary residence, it is protected from many judgment creditors. However, the deed does not by itself provide “asset protection” for your beneficiaries; once they inherit the home, it may become subject to their creditors unless another planning tool, such as a properly drafted trust, applies.

What happens if the beneficiary dies before the owner?

This is a critical risk of DIY deeds. If a beneficiary passes away first, their interest may lapse, pass under survivorship language to the surviving named beneficiaries, pass to that beneficiary’s descendants, or create probate/title issues, depending on how the deed is drafted. A well-drafted deed should say what happens if a beneficiary predeceases the owner and should include survivorship and/or “contingent beneficiary” language to help prevent the property from falling back into the probate system.

Can I sell my house if I have already recorded a Lady Bird Deed?

Usually, yes. You retain an enhanced life estate with broad powers to sell, mortgage, revoke, or give away the property without asking the beneficiaries for permission or even notifying them, if those powers are clearly reserved in the deed. Specific transactions may still require lender, title-company, or closing-agent review.

How does this affect my "Save Our Homes" tax cap?

In Florida, a properly drafted Lady Bird Deed is generally not treated as a current “transfer of ownership” for property-tax purposes during the owner’s lifetime. Your assessment usually should not be uncapped merely because you recorded the deed, but post-death tax treatment may differ depending on the beneficiaries, homestead eligibility, and current property-appraiser rules.